If I Use Already Taxed Money in Traditional Ira and Conver to Roth Do I Need to Pay Taxes Again

Thinking about converting your retirement account to a Roth IRA? It's easy to see why the Roth IRA is so incredibly popular.

Contributions to a Roth IRA are made with income that has already been taxed, meaning there's no initial tax benefit, but the money you have in a Roth grows tax-free over time.

Roth IRAs don't come with Required Minimum Distributions (RMDs) at age 72 like a traditional IRA either, so you can continue letting your money grow until you're ready to access it.

When you do decide to take distributions from a Roth IRA, you won't have to pay income taxes on that money. You already paid income taxes before you contributed, remember?

These are the main benefits of a Roth IRA that set this account apart from a traditional IRA, but there are plenty of others. With all of this in mind, it's no wonder so many people try to convert their traditional IRA into a Roth IRA at some point during their lives.

But, is a Roth IRA conversion really a good idea? This kind of conversion can certainly be lucrative over time, but you should definitely weigh all the pros and cons before you decide.

Table of Contents

- When Would You Want to Convert to a Roth IRA?

- When Would You Not Want to Convert?

- Roth IRA Conversion Rules You Need to Know

- What is the Backdoor Roth IRA and How Does It Work?

- Modeling IRAs in Your Own Plan

- Steps to Convert an IRA to a Roth IRA

- Roth IRA Conversion Examples

- Summary

When Would You Want to Convert to a Roth IRA?

Converting an existing traditional IRA or another retirement account to a Roth IRA can make sense in many different situations, but not all the time. At the end of the day, the value of this investing strategy depends on your unique situation, your income, your tax bracket, and the financial goal you're trying to accomplish in the first place.

The most important detail to understand is that, when you convert another retirement account to a Roth IRA, you will have to pay income taxes on the converted amounts. It can make sense to pay these taxes now to avoid more taxes later on, but that depends a lot on your tax situation now and what your tax situation may be like later in life.

The main scenarios where converting to a Roth IRA can make sense include:

- You will likely be in a higher tax bracket than you are now. If you are finding yourself in an especially low tax bracket this year or simply expect to be in a much higher tax bracket in retirement, then converting a traditional IRA to a Roth IRA can make sense. By paying taxes on the converted funds now — while you're in a lower tax bracket — you can avoid having to pay income taxes at a higher tax rate once you reach retirement and begin taking distributions from your Roth IRA. (Not sure about your future tax brackets? Use the NewRetirement Planner to approximate your future taxable income, rates, expense and more. This comprehensive tool puts the power of planning in your own hands.)

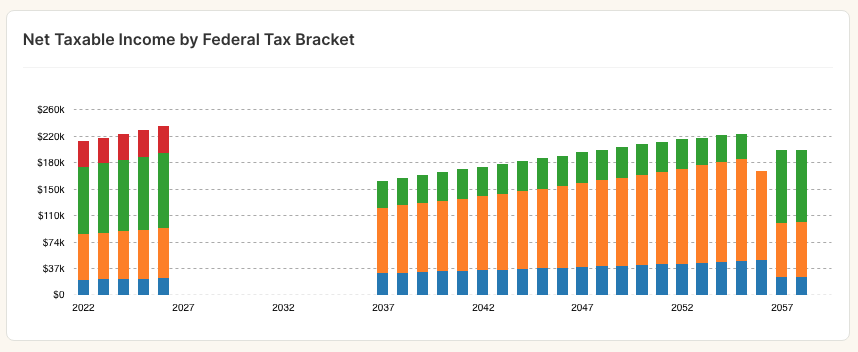

Lifetime tax prior to performing Roth conversions

- You have financial losses that can offset tax liability from the conversion. Converting another retirement account into a Roth IRA will require you to pay income taxes on the converted amounts. With that in mind, it can make sense to work on a Roth IRA conversion in a year when you have specific losses that can be used to offset your new tax liability.

- You don't want to begin taking distributions at age 72. If you don't want to be forced to take RMDs from your account at age 72, converting to a Roth IRA can also make sense. This type of account doesn't require RMDs at any age. (You can use the NewRetirement Planner to help you assess your income needs. See your taxable income for every future year and assess whether you need the income to cover expenses.)

- You're moving to a state with higher income taxes. Imagine for a moment you're gearing up to move from Tennessee — a state with no income taxes — to California — a state with income taxes as high as 12.3% In that case, it could make sense to convert other retirement accounts to a Roth IRA before you make the move and begin taking distributions.

- You want to leave a tax-free inheritance to your heirs. If you have extra retirement funds and worry about your heirs facing tax liability on an inheritance, converting to a Roth IRA can make sense. According to Vanguard, "the people who inherit your Roth IRA will have to take annual RMDs, but they won't have to pay any federal income tax on their withdrawals as long as the account's been open for at least 5 years."

These are just some of the instances where it can make sense to convert another retirement account into a Roth IRA, but there may be others. Also note that, before you do anything drastic or begin a conversion, it can be smart to speak with a tax advisor or financial planner with tax expertise.

At the very least, be sure to model the conversion as part of a comprehensive written retirement plan. The NewRetirement Planner enables you to try out specific conversion strategies in the context of your entire financial situation. Assess the conversion on your tax liability, net worth at longevity, and cash flow.

When Would YouNot Want to Convert?

Considering a Roth IRA conversion comes with immediate tax consequences, there are plenty of scenarios where doing one doesn't make any sense.

There are also plenty of personal situations where a Roth IRA conversion would likely go against a person's long-term goals. Here are some of the scenarios where a Roth IRA conversion could be a costly waste of time:

- You're going to have an extremely low income in retirement. If you have reason to believe you'll be in a much lower income tax bracket in retirement, then a Roth IRA conversion may not leave you better off. By not converting another retirement account to a Roth IRA, you can avoid paying taxes now at a higher rate for the conversion, and instead pay income taxes on your distributions at a lower rate in retirement.

- You don't have extra money for the conversion. Because converting another retirement account to a Roth IRA requires you to pay income taxes on those converted funds now, this move is a poor choice in years when you are short on extra money laying around to pay more taxes.

- You may need the money sooner rather than later. Withdrawals on money that was part of a Roth IRA conversion are subject to a five-year holding period. This means you would have to pay a penalty on that money if you chose to take distributions within a five-year period after the conversion.

Again, these are just some of the scenarios where you would want to think long and hard before converting another retirement account to a Roth IRA. There are plenty of other situations where this move wouldn't make any sense, and you should speak with a tax professional before you move forward either way.

Or, make sure you fully understand your projected income, expenses, and savings situation before doing a conversion. The NewRetirement Planner gives you detailed insight into all aspects of your financial future.

Roth IRA Conversion Rules You Need to Know

Though there are income limits that apply to contributing to a Roth IRA, these income limits do not apply to Roth IRA conversions. With that in mind, here are some important Roth IRA conversion rules you need to learn and understand:

Which accounts can you convert?

While the most common Roth IRA conversion is one from a traditional IRA, you can convert other accounts to a Roth IRA. Any funds in a QRP that are eligible to be rolled over can be converted to a Roth IRA.

60-day Rollover Rule

You can take direct delivery of the funds from your traditional IRA (check made payable to you personally), and then roll them over into a Roth IRA account, but you must do so within 60 days of the distribution. If you don't, the amount of the distribution (less non-deductible contributions) will be taxable in the year received, the conversion will not take place, and the IRS 10% early distribution tax penalty will apply.

Trustee-to-Trustee Transfer Rule

This is not only the easiest way to work the transfer but it also virtually eliminates the possibility that the funds from your traditional IRA account will become taxable. You simply tell your traditional IRA trustee to direct the money to the trustee of your Roth IRA account, and the whole transaction should proceed smoothly.

Same Trustee Transfer

This is even easier than a trustee-to-trustee transfer because the money stays within the same institution. You simply set up a Roth IRA account with the trustee who is holding your traditional IRA, and direct them to move the money from the traditional IRA into your Roth IRA account.

Additional Details to Be Aware Of

Note that, if you don't follow the rules outlined above and your money doesn't get deposited into a Roth IRA account within 60 days, you could be subject to a 10% penalty on early distributions as well as income taxes on the converted amounts if you're under the age of 59 ½.

And, as we already mentioned, you'll have to pay income taxes on converted amounts regardless of which rule you choose to follow above. You'll report the conversion to the IRA on Form 8606 when you file your income taxes for the year of the conversion.

What is the Backdoor Roth IRA and How Does It Work?

If your income is too high to contribute to a Roth IRA outright, the Backdoor Roth IRA offers a potential workaround. This strategy has consumers invest in a traditional IRA first since these accounts don't come with income limitations in terms of who can contribute. From there, a Roth IRA conversion takes place, letting those high-income investors take advantage of tax-free growth and future distributions without having to pay income taxes later on.

A Backdoor Roth IRA can make sense in the same scenarios any Roth IRA conversion makes sense. This type of investment strategy intends to help you save money on taxes later at the cost of higher taxes now, in the year you make the conversion.

The big disadvantage of a Backdoor Roth IRA is a whopping tax bill, you're hoping to lower your tax liability in the future. That's a noble goal but, once again, the Backdoor Roth IRA only makes sense in situations where tax savings can truly be realized.

Modeling IRAs in Your Own Plan

Interested in a Roth IRA, but aren't sure if it is right for you? Try modeling it in your own plan.

The NewRetirement Planner is the most powerful and comprehensive modeling tool available online. It's for people who want clarity about their choices today and their financial security tomorrow. It gives people the ability to discover, design, and manage personalized paths to a secure future. Helping you make smart decisions about your money, including whether or not you should do a Roth conversion, is the heart of the tool.

You have two options for how to model conversions in the NewRetirement Planner:

Model Individual Conversions

Once you have set up all aspects of your plan (a really thorough inventory of your current and future income, expenses, and savings), you can try modeling a specific conversion that you think would be advantageous.

- In Money Flows, you can specify the account from which the money will be withdrawn, the amount you wish to convert, the age when you want to do the conversion, and your projected rate of return on the converted money.

- Once saved, you can immediately see if the conversion resulted in a change to your out of savings age, estate value, or lifetime tax liability.

- And, you can review charts to assess your tax liability in the year you do the conversion, the impact on income from RMDs, and more.

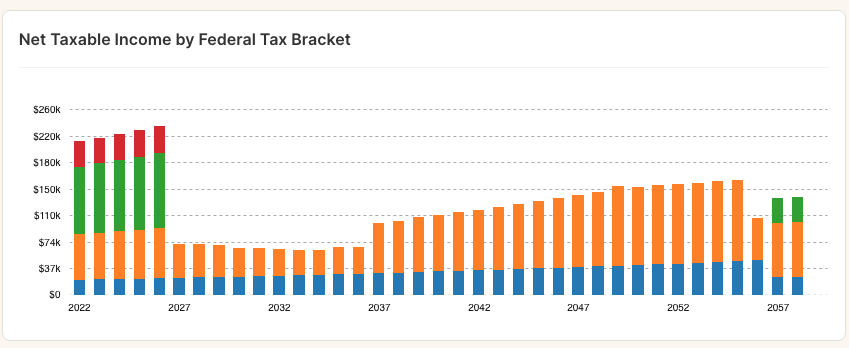

Lifetime tax after performing Roth conversions

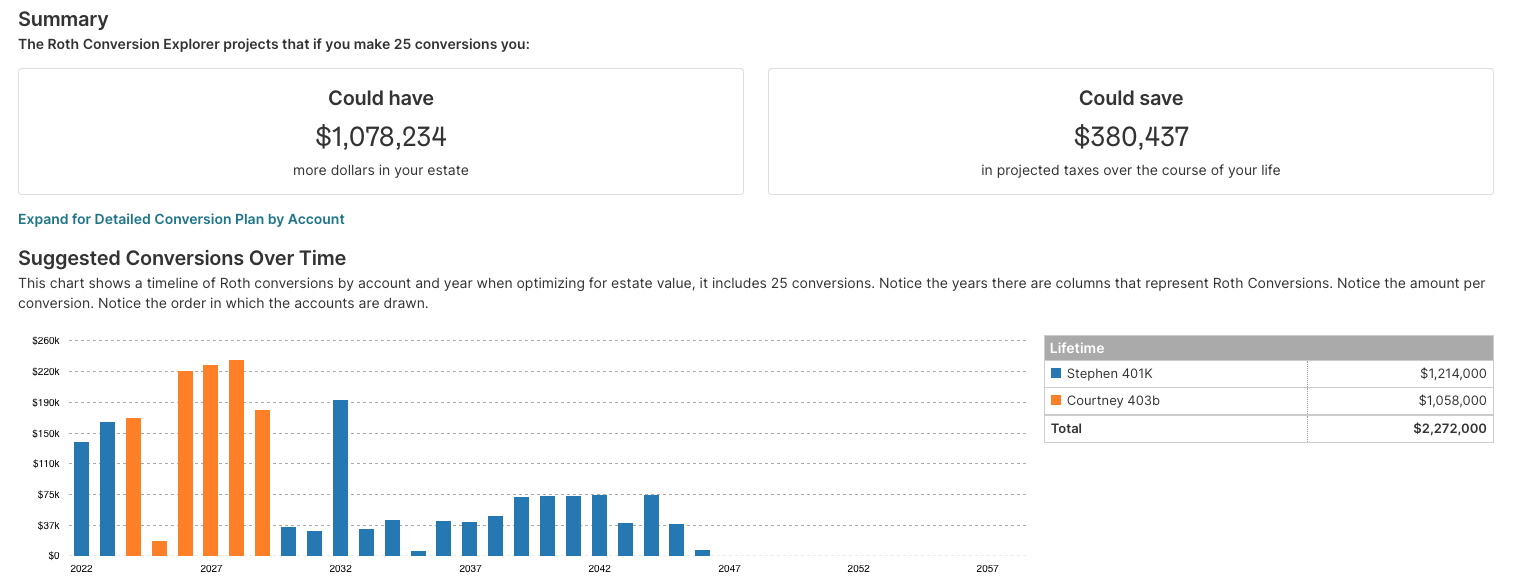

Use the Roth Conversion Explorer

The Roth Conversion Explorer is a modeling tool within the NewRetirement Planner.

If you are not sure when or if you should do a Roth conversion, you might start with this tool. It will analyze all aspects of your plan, running hundreds of scenarios, to generate a conversion strategy that could increase your estate value at your longevity.

Steps to Convert an IRA to a Roth IRA

If you think a Roth IRA conversion would be a good move on your part, here are the steps you'll want to take.

1. Open a Roth IRA

First, make sure you open a Roth IRA with one of the top brokerage firms. We think TD Ameritrade is one of the best Roth IRA providers out there due to the fact you pay $0 per trade and $0 per year. However, you should also check out top Roth IRA providers like Betterment, Ally, LendingClub, and Vanguard.

![]()

- $0 per trade

- $49.99 mutual fund

- Annual:$0

- Minimum:$0

2. Transfer Existing IRA Assets to the Roth IRA

Next, you'll want to initiate a Roth IRA conversion with your traditional IRA or QPR provider. Remember that, if you choose to accept the funds with a check, you have 60 days to move the money into your Roth IRA account. You can also have the funds moved via a trustee to trustee transfer or even using the same brokerage account, and this is often easier since the move should theoretically be taken care of on your behalf.

3. Pay Income Taxes On the Conversion

The major downside of a Roth conversion is that you will be paying taxes on the amount converted in the current year, and depending on your income tax bracket and the amount you're converting, the tax bite could be substantial. With that being said, you will hopefully plan your conversion in a year when you're in a lower tax bracket, or when you have other losses you can use to offset additional taxes caused by the conversion.

Roth IRA Conversion Examples

Whenever you're dealing with numbers, it's always helpful to demonstrate the concept with examples. Here are two real-life examples that I hope will illustrate how the Roth IRA conversion works in the real world.

Example 1

Parker has a SEP IRA, a Traditional IRA, and a Roth IRA totaling $310,000. Let's break down the pre-and post-tax contributions of each:

- SEP IRA: Consists entirely of pre-tax contributions. Total value is $80,000 with pre-tax contributions of $12,000.

- Traditional IRA: Consists entirely of after-tax contributions. Total value is $200,000 with after-tax contributions of $40,000.

- Roth IRA: Obviously all after-tax contributions. Total value is $30,000 with total contributions of $7,000.

Parker is wanting to only convert half of the amount in his SEP and Traditional IRA to the Roth IRA. What amount will be added to his taxable income in 2022?

Here's where the IRS pro-rata rule applies. Based on the numbers above, we have $40,000 in total after-tax contributions to non-Roth IRA. The total non-Roth IRA balance is $280,000. The total amount that is desired to be converted is $140,000.

The amount of the conversion that won't be subject to income tax is 14.29%; the rest will be. Here's how that is calculated:

Step 1: Calculate non-taxable portion of total Non-Roth IRA's: Total after-tax contributions / Total Non-Roth IRA Balance = Non-Taxable %:

$40,000 / $280,000 = 14.29%

Step 2: Calculate the non-taxable amount by converting the result to Step 1 into dollars:

14.29% x $140,000 = $20,000

Step 3: Calculate the amount that will be added to your taxable income:

$140,000 – $20,000 = $120,000

In this scenario, Parker will owe ordinary income tax on $120,000. If he is in the 22% income tax bracket, he will owe $26,400 in income taxes, or $120,000 x .22.

Example 2

Bentley is over the age of 50 and in the process of changing jobs. Because his employer had been bought out a few times, he has rolled over his previous 401k into two different IRAs.

One IRA totals $115,000 and the other consists of $225,000. Since he's never had a Roth IRA, he's considering contributing to a nondeductible IRA for a total of $7,000 and then immediately converting in 2022.

- Rollover IRA's: Consists entirely of pre-tax contributions. Total value is $340,000 with pre-tax contributions of $150,000.

- Old 401k: Also consists entirely of pre-tax contributions. Total value is $140,000 with $80,000 pre-tax contributions.

- Current 401k: Plans out maxing it out for the rest of his working years.

- Non-deductible IRA: Consists entirely of after-tax contributions. Total value will be $7,000 of after-tax contributions and we will assume no growth.

Based on the above information, what will be Bentley's tax consequence in 2022?

Did you notice the curveball I threw in there? Sorry – I didn't mean to trick anybody – I just wanted to see if you caught it. When it comes to converting, old 401(k)s and current 401(k)s do not factor into the equation. Remember this if you are planning on converting large IRA balances and have an old 401(k). By leaving it in the 401(k), it will minimize your tax burden.

Using the steps from above, let's see what Bentley's taxable consequence will be in 2022:

- Step 1: $7,000/ $346,000 = 2.02%

- Step 2: 2.02 X $7,000 = $141

- Step 3: $7,000 – $141 = $6,859

For 2022, Bentley will have a taxable income of $6,859 of his $7,000 Traditional IRA contribution/Roth IRA conversion, and that's assuming no investment earnings. As you can see, you have to be careful when initiating the conversion.

If Bentley had gone through with this conversion and didn't realize the tax liability, he would need to check out the rules on recharacterizing his Roth IRA to get out of those taxes.

Examples are useful, but what is right for you?

Using these examples, it is time to try modeling Roth conversion as part of your own financial future. The NewRetirement Planner enables you to run different scenarios and see the impact on your finances.

Summary

If you meet certain criteria and don't mind facing a larger than average tax bill during the conversion year, a Roth IRA conversion could absolutely make sense.

However, you should absolutely weigh the pros and cons of this move before you pull the trigger, and you should definitely set aside the time to speak with a professional who can help you walk through the tax implications.

A Roth IRA conversion can help you avoid taxes later in life when you would really benefit from some tax-free income, but don't jump in blindly. Research everything you can about Roth IRA conversions and alternative ways to save more for retirement, and make sure any decision you make is an informed one.

adamswoustravight.blogspot.com

Source: https://www.goodfinancialcents.com/roth-ira-conversion-tax-rules/

0 Response to "If I Use Already Taxed Money in Traditional Ira and Conver to Roth Do I Need to Pay Taxes Again"

Post a Comment